A key risk factor I discovered dealing with thousands of failed contractors was that these contractors failed to use business science tools to manage their business and were often surprised and angry when they suddenly ran out of cash and had to close the doors.

If these contractors had been using available business tools they would not have suddenly run out of cash and failed. They would have been better informed and able to take corrective action. It always puzzled me why they didn’t use financial engineering to manage their business as they used construction engineering to build their projects?

This current series of messages is not meant to be a primer on preparing financial statements. Rather, I am trying to offer contractors a deeper insight into how they might use the tools of business science to build their companies and minimize the profound financial risks inherent in the construction transaction.

Financial ‘Engineering’

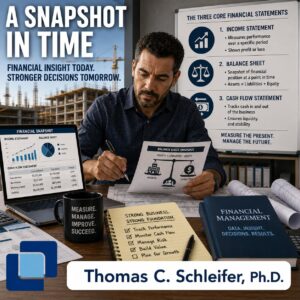

We are all familiar with the three core financial statements: the income statement, the balance sheet, and the cash flow statement. Together, they provide a complete picture of a company’s financial health by tracking profitability, net worth, and cash movement over time. A thorough understanding of how to use these scientific financial statements would have prevented the thousands of contractor failures I was called in to salvage.

1. Income Statement

Also known as a Profit and Loss (P&L) statement, measures a company’s financial performance over a specific period.

- Key Components: Revenues (sales) minus expenses (costs of goods sold, operating expenses, and taxes) to calculate net income. The key to this document’s integrity is the exact matching of income and expenses within a designated period of calendar time (month, quarter, year).

- Primary purpose: To show whether the company is operating at a profit or a loss.

- Construction Industry Problem: The revenue or income is earned in progress payments paid intermittently over the project’s time frame. During the lifetime of a project, it is impossible to exactly match partial revenue earned to the applicable expenses within the confines of a traditional calendar period. The revenue earned can only be estimated leaving the match of expenses to that estimated revenue an estimation as well. We are left with two estimated variables to calculate exact income. Impossible.

2. Balance Sheet

This provides a “snapshot” of a firm’s financial position at an exact moment in time.

- Key Components: Assets (what the company owns), Liabilities (what it owes), and Shareholders’ Equity (the net worth left for owners).

- Core Equation: {Assets} = {Liabilities} + Equity).

- Primary purpose: Show the firm’s net worth, its overall leverage and liquidity.

3.Cash Flow Statement

This tracks the actual movement of cash and cash equivalents in and out of a business over a specific period.

- Key Components: Cash generated or used in Operating, Investing, and Financing activities.

- Primary purpose: To determine if the company has enough liquid cash to pay its bills, fund operations, and grow.

A Snapshot in Time

Last week I explained how the magical science of “double entry bookkeeping” produces a snapshot of your company’s financial status at any moment in time. An analysis of this snapshot can offer several useful insights. Remember, for the balance sheet to ‘balance,’ assets must equal liabilities plus equity.

- This “balancing” is supposed to ensure that every financial transaction and its impact on liquidity is trapped inside this equation and matched within the specified time frame. Nothing should be able to escape its notice.

- In addition to tracking liquidity the assets minus liabilities equation states the equity of the firm. If the equity is increasing over time, the contractor can be assured that the completed projects did indeed contribute profitability to the firm. This is the best way to clear up the fuzziness of the ongoing profit and loss “estimates” that often mislead contractors into thinking they’re operating profitably when in fact, they’re losing money and are in for a surprise.

- A look at the total capital of the firm which analyzes liabilities and equity together, gives contractors their best feel for the current financial heft of their firms and the size jobs they might be able to tackle in the future.

- There are a variety of ratios contractors can use to gauge the efficiency of their company’s balance sheet. Some of the most common include asset turnover, the quick ratio, receivables turnover, debt to assets, and debt to equity, (All of these will be further explained in next week’s blog).

- Comparing two balance sheets at different moments in time creates the Cash Flow Statement which basically tells contractors where they used cash during the last accounting period and how much they have left to run their business in the future.

Next Week

Next week we’ll delve a little deeper together into how these financial statements can be used to better manage a complex construction company. (Note: Contractors are not accountants. Readers not fully understanding the accounting concepts mentioned here should get clarification from their accountant before the next Blog Message.)

For more information on construction accounting, read more at: ACCOUNTING

For a broader view of financial statements, read more at: STATEMENTS

To receive the free weekly Construction Messages, ask questions, or make comments contact me at research@simplarfoundation.org.

Please circulate this widely. It will benefit your constituents. This research is continuous and includes new information weekly as it becomes available. Thank you.